Registered Education Savings Plans (RESPs) have become essential for Canadian families’ education planning. With the price of post-secondary education rising steadily, understanding the mechanics and nuances of RESP withdrawals is more critical than ever. Knowing the RESP withdrawal rules helps families avoid costly mistakes, maximize available funding, and ensure students can access all the support these accounts offer.

RESPs are intentionally nuanced structures built to encourage long-term savings. Subscribers need to understand the different account components, recent legislative changes, and the tax implications associated with withdrawals to access their full advantages. The government provides incentives to maximize educational savings, but to reap these rewards, parents and students need to plan withdrawal strategies carefully to adapt to changing educational costs.

RESPs are unique compared to other savings vehicles because eligibility for grants, tax-advantaged growth, and withdrawal limits all benefit the student, but only if used properly. Navigating RESP withdrawals intelligently is a cornerstone of sound education planning and helps ensure students have access to the funding they need throughout their academic journeys.

Families should regularly review RESP policies and consult reputable sources on government programs that impact education funding to stay informed about their rights and options. Staying up-to-date enables optimal decision-making and reduces the likelihood of stressful or costly errors that could affect a student’s future. Families can consult trusted sources like the Government of Canada’s RESP guide for more guidance.

Understanding RESP Components

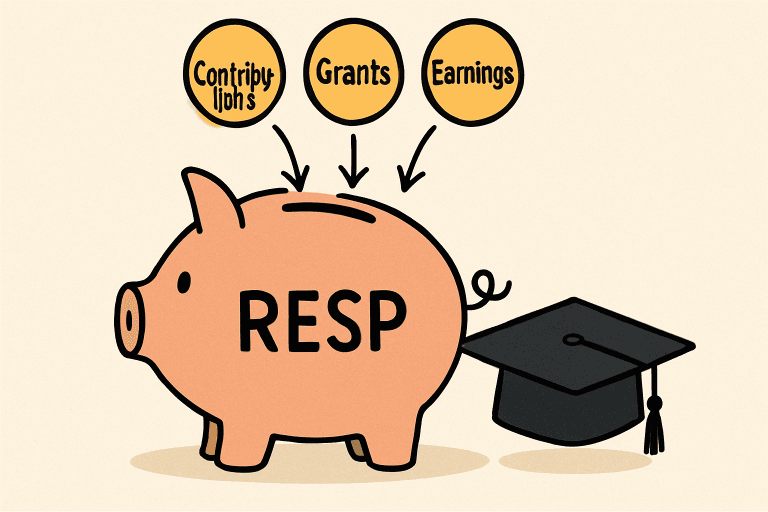

An RESP is comprised of three distinct financial streams:

- Contributions: These are the after-tax dollars a subscriber—typically a parent or guardian—deposits into the account. They are not taxed upon withdrawal.

- Government Grants: The RESP attracts incentives such as the Canada Education Savings Grant (CESG) and, for eligible families, the Canada Learning Bond (CLB). These grants can add substantial value to the original savings.

- Investment Earnings refer to the income or growth generated from the funds invested inside the RESP. Investment growth and government grants are taxable but only when withdrawn as EAPs.

Each component comes with unique withdrawal rules, making it essential to distinguish among them when developing an education savings strategy.

Types of RESP Withdrawals

RESP withdrawals are categorized into two main types, each serving a different purpose in supporting a student’s academic journey:

- Post-Secondary Education Payments (PSE): PSE withdrawals draw only from the subscriber’s original contributions. These payments are not taxed, and there are no restrictions on timing or amount—once a student enrolls in an eligible post-secondary program, funds can be used for any need.

- Educational Assistance Payments (EAP): EAPs tap into government grant money and all accumulated investment earnings. These withdrawals are taxable to the student, who is often in a low or zero tax bracket, so the practical tax impact is usually minimal.

Students must provide proof of enrollment when making RESP withdrawals to ensure eligibility and compliance with federal regulations.

Recent Changes to EAP Withdrawal Limits

As education expenses have soared recently, the Canadian government announced key RESP reforms to address funding gaps. Since 2023, full-time students can access up to $8,000 in EAP funds (up from $5,000) during the first 13 weeks of post-secondary enrollment, while part-time students can withdraw up to $4,000 (up from $2,500). These increases offer families more flexibility and reflect students’ escalating up-front costs in their early semesters, including tuition, housing, and textbooks. For more, see this coverage of EAP changes.

Tax Implications of RESP Withdrawals

Tax treatment is a key element of RESP planning. The principal (PSE) is always tax-free upon withdrawal. In contrast, EAPs represent taxable income for the student, though taxation is typically low because most students’ total incomes are modest during college or university. To enhance tax efficiency, families should map out a multi-year withdrawal plan, spreading EAP withdrawals over the student’s academic tenure to avoid pushing them into a higher tax bracket in any single year.

Strategic Withdrawal Planning

Careful withdrawal planning is a must to get the most value from an RESP. Here are strategies to ensure families maximize the available benefits:

- Prioritize EAP Withdrawals First: Use grant and investment earnings early since they are subject to withdrawal limits and taxation. EAPs must be used for eligible expenses, and unused grant portions may need to be returned if not withdrawn.

- Monitor Student Income: If the student has part-time employment or other sources of income, spread EAP withdrawals over multiple years to avoid increased taxable income in a single year.

- Plan for Unused Funds: If the beneficiary decides not to enroll in post-secondary education, it is possible to transfer the RESP to another eligible beneficiary or roll up to $50,000 into an RRSP, provided there is contribution room and certain conditions are met.

Common Mistakes to Avoid

Mistakes such as withdrawing funds before confirming student enrollment or failing to submit the required documentation can result in grant repayment or unintended taxes. Families should also avoid neglecting to use EAP funds for eligible expenses, as unused grants may ultimately have to be returned to the government. Consulting financial advisors or education planning specialists and staying informed about regulatory updates can help families avoid these pitfalls.

Conclusion

RESPs provide a powerful platform for building a secure educational future, but their real value is unlocked only through careful, informed withdrawal planning. Understanding the rules, keeping abreast of recent policy changes, and deploying strategic withdrawal methods will help families make the most of every dollar saved and every grant received on the journey to post-secondary education.